$165B Project Jupiter, New Mexico

Jupiter is not only the largest planet, but also a massive data center project in New Mexico.

Data centers. They are powering the construction industry with their deliverables – AI and storing / managing data for businesses and consumers – powering the economy. They started in the billion-dollar range, grew to 10s of billions, and now they are in the $100+ billion mega projects.

And their massive size is absorbing labor as well as selected supplies, exasperating shortages in both.

Project Jupiter video – https://vimeo.com/1152644123?fl=pl&fe=vl

Bob Allomong, and HVAC independent manufacturer rep who writes for our HVACRTrends site, recently shared information for a mega project in New Mexico called Project Jupiter. It is a $165 billion data center project. It has its own website (and check out the construction video.)

And it’s in a state whose 2025 projected private commercial construction expenditures was $3 billion!

At the recent NAED’s I had a few manufacturers ask me for thoughts on data centers and if I thought that the boom may decline / stop in the near future? My response was no given the future of the economy – more online, more AI (more people to use, current users using it more), autonomous vehicles, robotics, and quantum computing to name a few emerging concepts let alone that more data and more electronic transactions are generated every day that need to be stored.

Will the growth rate slow? Yes, but that is a math issue as there are more data centers in the market. The nature will also change as the building format may not change but the insides will. So “construction” for the “box” (building) may slow but the spend inside will continue (similar to an industrial facility … the construction isn’t needed but there is MRO spend an occasional CapEx for overhauls and expansion of lines.)

Bob’s article touches on a number of issues with a focus on labor concerns (usage of New Mexico labor and how much needs to be brought in … they only need 4,000 skilled workers!)

I’ve edited some of it and the complete article can be found on HVACRTrends.

“In today’s trades environment, risk doesn’t live in headlines—it shows up in execution.

- It appears as margin compression on fixed bids.

- As delayed timelines when materials don’t arrive.

- As missed opportunities when labor isn’t available.

And increasingly, it shows up in how large-scale projects—especially headline-grabbing developments—actually translate into real, measurable outcomes for the skilled trades.

Few projects illustrate this more clearly than Project Jupiter in southern New Mexico.

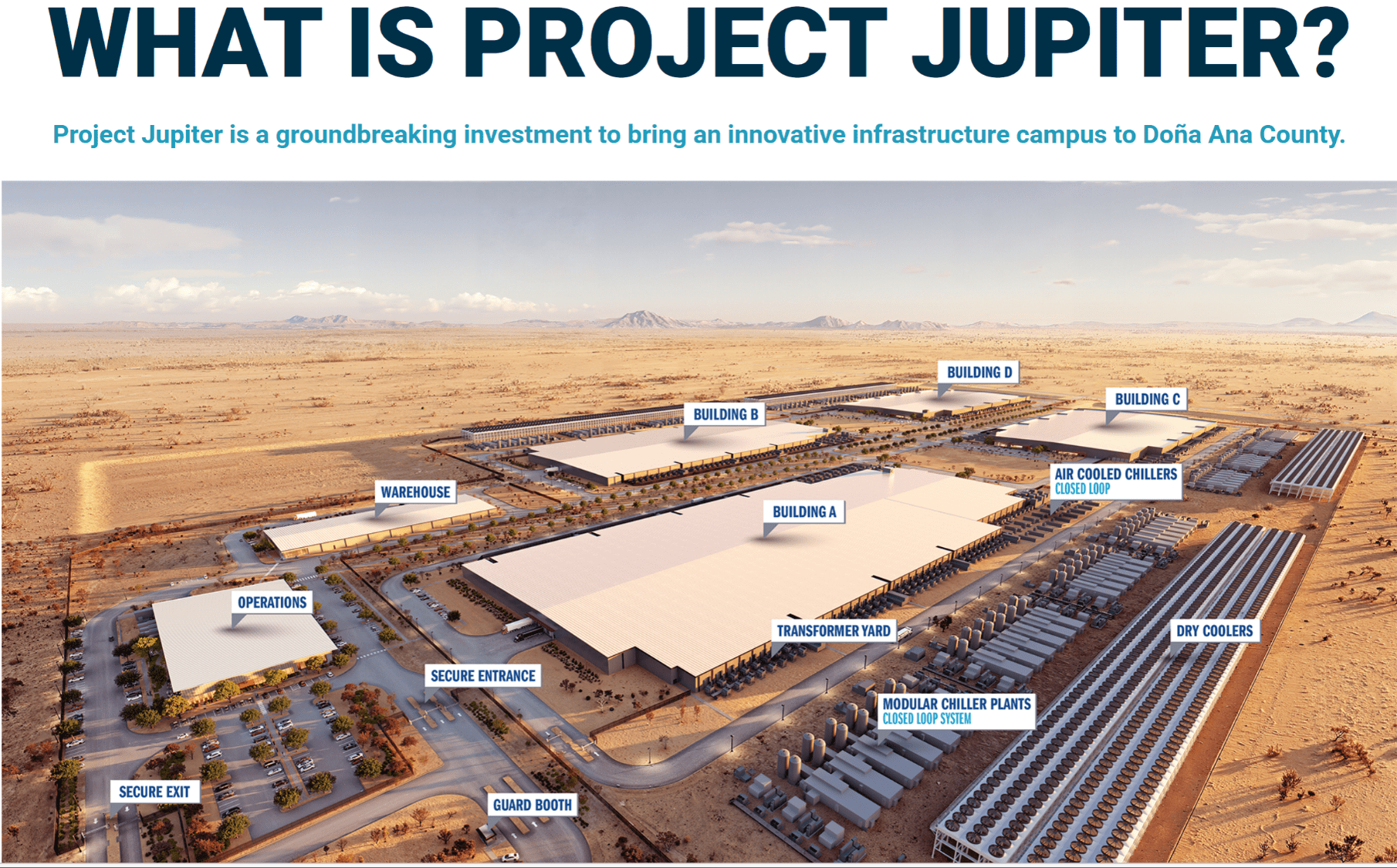

A $165 Billion Bet — What Project Jupiter Actually Is

For those outside the region, Project Jupiter requires some context.

The proposed development is a $165 billion data center campus near Sunland Park, New Mexico—positioned as one of the largest private investments in state history and a major step into the rapidly expanding AI and data infrastructure economy.

It’s been described as:

- A transformational economic catalyst.

- A gateway into next-generation technology infrastructure.

- A once-in-a-generation opportunity for the region.

And to be fair, local and state leaders have treated it that way.

Doña Ana County approved massive Industrial Revenue Bonds tied to the project, effectively offering long-term tax advantages to developers. The deal was fast-tracked, supported aggressively, and pushed forward despite public concerns around water usage, transparency, and long-term impact.

In simple terms: New Mexico didn’t hesitate. They cleared the runway for a $165 billion development.

But that raises a more important question: Will the value of that $165 billion actually reach the tradespeople who build it?

Strip Away the Hype — This Is a Trades Project

Despite the AI branding and tech-driven narrative, Project Jupiter is fundamentally something much more familiar: A construction project.

At full scale, it will depend entirely on skilled labor:

- Electricians installing extensive power infrastructure.

- HVAC/R technicians building precision cooling systems.

- Pipefitters and welders assembling critical systems.

- General labor bringing the site to life.

This isn’t a side note to the project—it is the project.

Which makes the stakes clear: if the local New Mexico trades aren’t meaningfully included, the economic impact narrative breaks down. (Note – Bob is based in New Mexico, so you can understand his concern. In reality, much of the labor will come in from out of state. As someone said recently – “they need pop-up motels / hotels like they used to have in the Dakotas.”)

How Risk Actually Shows Up

Projects like this are often framed in macro terms—investment size, job creation projections, long-term economic impact. But in the trades, risk is more practical.

It shows up as:

- Tightened margins when material costs shift mid-project.

- Compressed timelines due to supply chain delays.

- Increased competition for limited labor.

- Pressure to move faster, often at the expense of process.

These are not theoretical challenges—they are daily operational realities.

And they all converge into a single constraint.

The Real Bottleneck: Execution Capacity

You can hedge commodities. You can diversify suppliers. You can structure favorable financing.

But if you don’t have the workforce, systems, and operational capacity to execute—none of it matters.

Execution capacity is the ultimate limiting factor.

In an undertaking like Project Jupiter, that constraint becomes even more pronounced.

At peak construction, demand for skilled labor will surge. Thousands of workers will be needed across multiple trades, often simultaneously. Contractors will be asked to scale quickly, coordinate complex scopes, and deliver under tight timelines.

And if the local market can’t meet that demand?

The outcome is predictable:

- Outside labor fills the gap.

- External firms capture high-value scopes.

- Local participation becomes secondary.

The Three-Year Window That Changes Everything

One of the most important—and least discussed—aspects of Project Jupiter is its timeline.

The bulk of construction is expected to occur over a relatively short window:

approximately 2025 through 2028.

That’s when:

- Job availability peaks.

- Wages rise due to demand.

- Opportunities for contractors expand.

But after that window closes, the dynamic shifts quickly.

Data centers are not labor-intensive in operation. Once construction is complete, workforce needs drop significantly. Facilities transition to lean operational teams, not large construction crews.

This creates a critical reality for the trades: The opportunity is massive—but temporary.

From Managing Inputs to Owning Them

Historically, many trades businesses have focused on managing inputs:

- Negotiating better material pricing.

- Running lean inventory.

- Adjusting labor reactively.

That approach worked in more stable conditions.

Today, leading companies are moving toward something more proactive: Owning their inputs.

This shift is happening across three key areas:

1). Workforce.

Labor is no longer just a cost—it’s the defining constraint.

Resilient companies are:

- Building apprenticeship pipelines.

- Partnering with trade schools.

- Cross-training technicians.

- Planning capacity ahead of demand.

In a project like Project Jupiter, workforce readiness will determine who participates—and who gets left out.

2). Supply Chain.

The just-in-time model is giving way to the concept of strategic redundancy.

Companies are:

- Dual-sourcing critical materials.

- Carrying safety stock on key components.

- Strengthening distributor relationships.

This reduces vulnerability when disruptions occur.

3). Customer and Project Mix.

Diversification matters more than ever.

Contractors are:

- Balancing service work with large projects.

- Targeting funded or grant-backed opportunities.

- Avoiding overexposure to a single segment.

This provides stability in volatile conditions.

The Shift from Lean to Resilient by Design

For years, efficiency meant minimizing operational excesses.

- Lean inventory.

- Minimal overhead.

- Tight labor utilization.

But volatility has changed the equation.

We are now seeing a shift from “lean” to “resilient by design.”

That means:

- Carrying more inventory to avoid costly delays.

- Investing in labor ahead of demand.

- Building redundancy into operations.”

And the complete article can be found on HVACRTrends, or email me as Bob expresses comments regarding labor concerns as well as implications for local markets.

The Data Center Opportunity

- The data center opportunity continues to be huge … to the winners. In New Mexico you can envision Summit Electric (Sonepar), Wesco, Graybar being the primary winners due to project / order sizes and proximity. For selected manufacturers … ask about continued backlogs.

- The electrical opportunity is typically 40-45% of the construction spend, however, much is direct. The gray goods element, which is electrical construction spend, is significantly lower.

- Late last year, Channel Marketing Group and DISC partnered to publish a data center research report, which was spearheaded by CMG’s Kevin Coleman. This 25-page report hints at the opportunity, provides some electrical industry benchmarks and shares more. Click here to learn more about the report and here to purchase it for $199.

$165B! Over 4 years!

Trending Now

Project Jupiter - $165B Data Center

You may also like